Categories

Home Buyers, Home SellersPublished June 5, 2026

What Rising Inflation Means for Your Move: A Housing Market Reality Check for 2026

Are rising inflation and the possibility of higher interest rates a reason to delay your move?

Not necessarily. While inflation has recently accelerated and mortgage rates may remain elevated longer than expected, today's housing market is fundamentally different from past downturns. Understanding what's happening can help you make a confident decision based on your goals, not just the headlines.

Inflation Is Rising Again. Here's What's Happening.

Inflation has become one of the biggest economic stories of 2026.

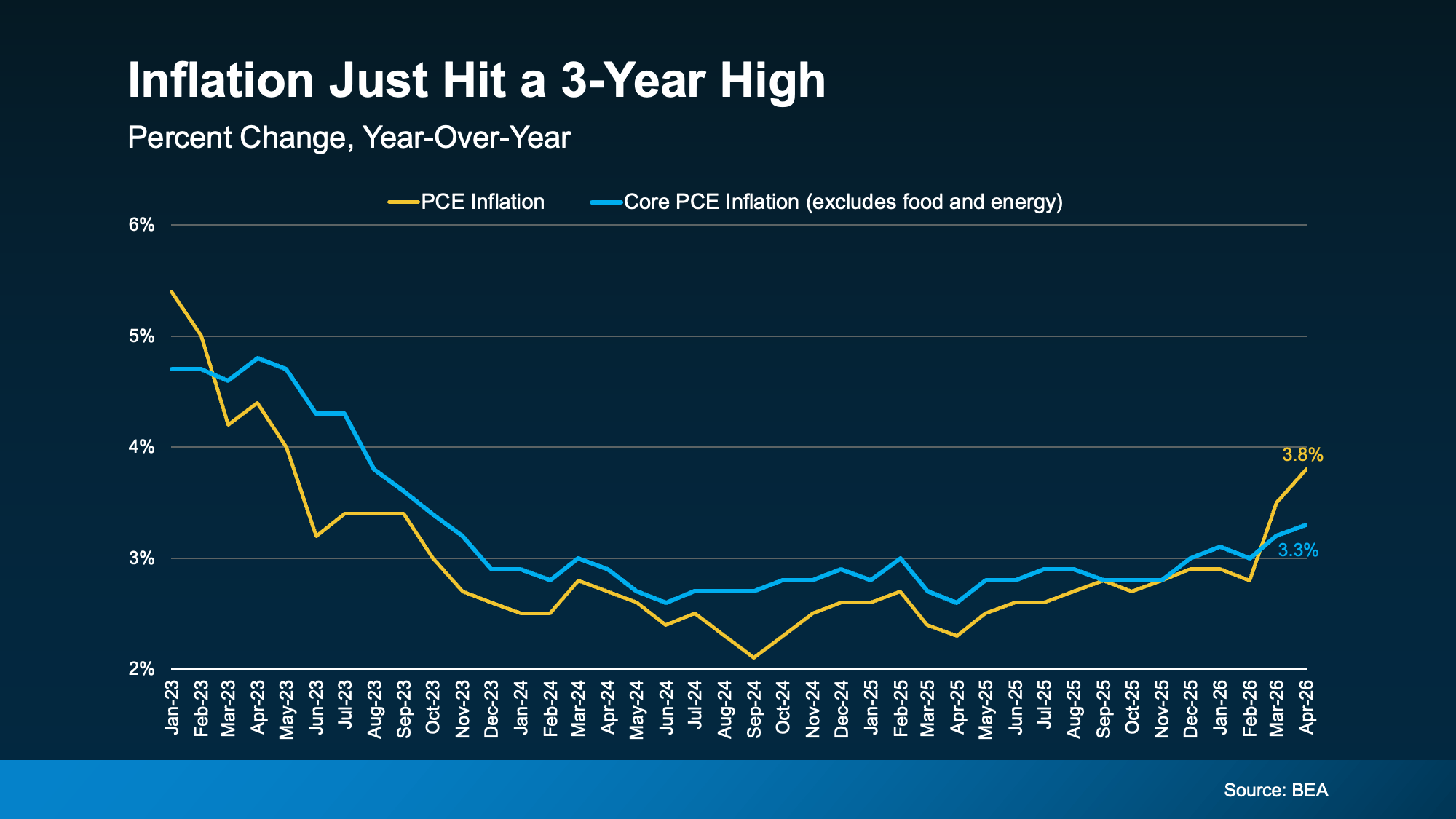

The latest Personal Consumption Expenditures (PCE) data, one of the Federal Reserve's preferred inflation gauges, shows inflation reaching a three-year high. Much of the recent increase has been driven by rising energy costs and geopolitical uncertainty, particularly disruptions affecting global oil markets.

Inflation Trend

Looking deeper into the data reveals an important distinction.

The yellow line represents overall PCE inflation, which includes energy and food costs. The blue line represents Core PCE inflation, which excludes those volatile categories.

While both have increased, Core PCE has risen much more gradually.

That's significant because it suggests the recent spike is being driven largely by external factors, particularly energy prices, rather than widespread inflation throughout the economy.

For consumers, that doesn't necessarily make higher prices feel any better. But for economists and policymakers, it provides valuable context about where inflation pressures are coming from.

Why Inflation Matters to Home Buyers

When inflation rises, the Federal Reserve often responds by maintaining higher interest rates or raising them further.

Their goal is simple: slow spending enough to bring inflation back under control.

While mortgage rates aren't directly tied to the Federal Funds Rate, they are heavily influenced by the same economic forces that drive Fed policy.

When investors expect inflation to remain elevated, mortgage rates often stay higher as well.

For buyers hoping rates would decline significantly this year, the latest inflation data suggests that timeline may be delayed.

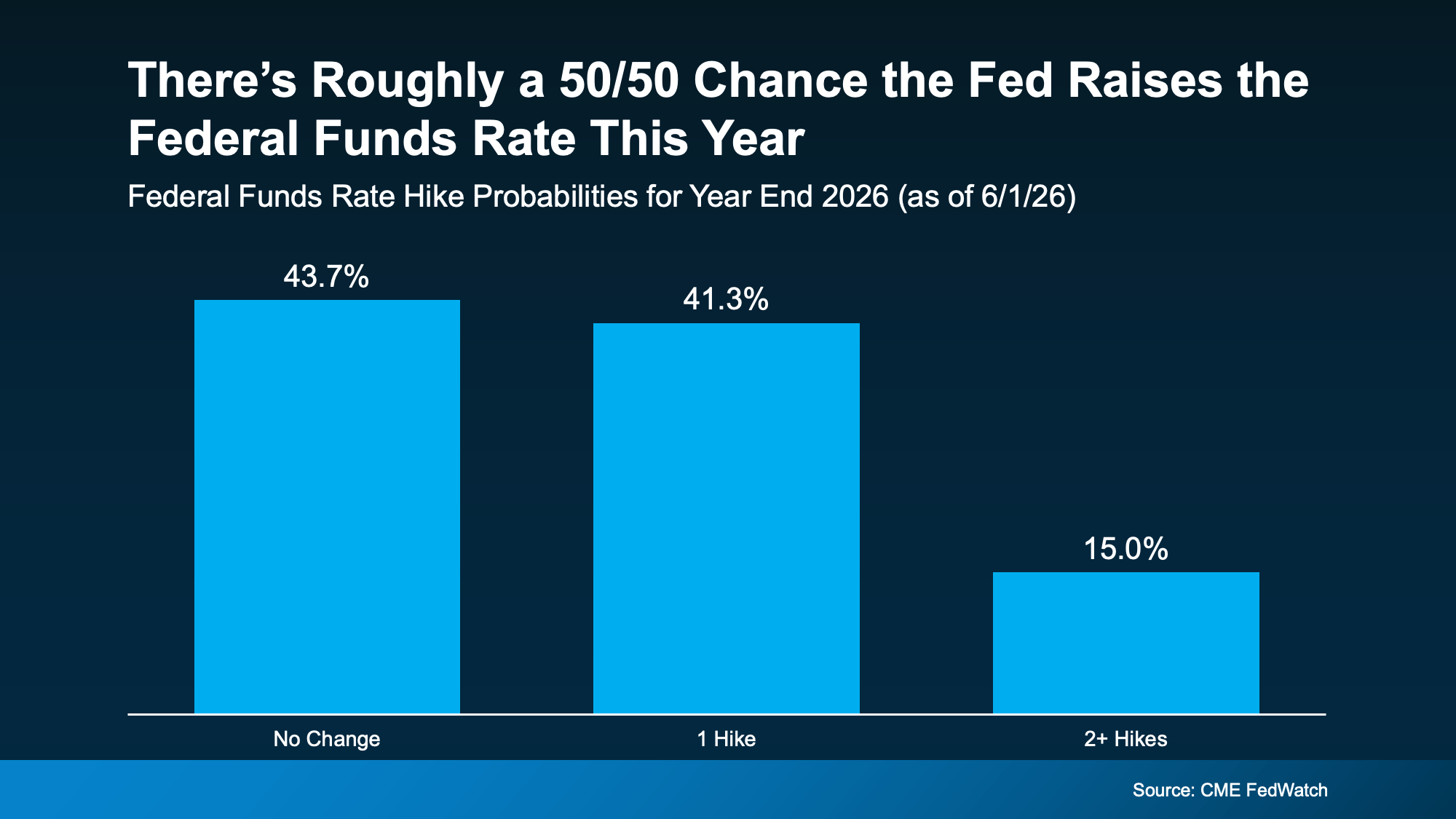

Could the Fed Raise Rates Again?

According to current market expectations, the answer is: maybe.

Federal Funds Rate Outlook

Current futures market projections suggest:

- Approximately 44% probability of no change

- Approximately 41% probability of one rate increase

- Approximately 15% probability of multiple increases

In other words, the market sees nearly equal odds that the Fed could raise rates before the end of the year.

That uncertainty matters because it reinforces a key message many buyers don't want to hear:

Mortgage rates may stay higher for longer.

While no one can predict exactly where rates will go, waiting solely for a dramatic drop could leave some buyers sitting on the sidelines longer than expected.

What This Means for Home Sellers

If you're selling, rising inflation affects your strategy too.

Higher borrowing costs can impact affordability for buyers, which means pricing accurately becomes even more important.

Today's buyers are:

- More payment-sensitive

- More selective

- More focused on value

That doesn't mean homes aren't selling.

It means presentation, pricing, marketing, and negotiation matter more than they did during the ultra-competitive market of 2021 and 2022.

The good news is inventory remains relatively constrained in many markets, helping support overall home values.

Why This Is Nothing Like 2008

Whenever inflation rises and mortgage rates remain high, concerns about another housing crash tend to follow.

The comparison makes for dramatic headlines, but it doesn't align with today's housing fundamentals.

Inventory Remains Relatively Low

One of the primary drivers of the 2008 housing collapse was an oversupply of homes.

Today's market faces the opposite challenge.

Many markets continue to experience housing shortages that have developed over more than a decade of underbuilding.

While inventory has increased compared to recent years, we're still nowhere near the levels seen before the last crash.

Homeowners Have Significant Equity

Today's homeowners have built substantial equity.

Many purchased or refinanced during periods of historically low interest rates and have benefited from years of home appreciation.

This creates a financial cushion that simply didn't exist for many homeowners during the housing bubble.

Lending Standards Are Much Stronger

Before the financial crisis, lending practices were far looser.

Today, mortgage qualification requirements are significantly more rigorous.

Borrowers generally have:

- Better credit profiles

- Verified income

- Documented assets

- More sustainable debt-to-income ratios

That dramatically reduces systemic risk.

Affordability Is the Challenge

The biggest challenge facing today's market isn't distressed homeowners.

It's affordability.

Higher home prices combined with higher mortgage rates have increased monthly payments, creating hurdles for buyers.

That's a very different issue than widespread mortgage defaults.

Should Buyers Wait for Lower Rates?

This may be the most common question in real estate right now.

The answer depends less on the market and more on your personal circumstances.

Consider these questions:

- Do you need more space?

- Are you relocating for work?

- Has your family situation changed?

- Are you downsizing?

- Are you currently paying high rent?

If the answer to any of those is yes, waiting for a perfect market may not be the best strategy.

Life doesn't pause while the economy works itself out.

Many buyers are discovering that finding the right home matters more than perfectly timing mortgage rates.

Strategies Buyers Can Use Right Now

Even in a higher-rate environment, there are ways to improve affordability.

Explore Rate Buydowns

Some sellers and builders are offering concessions that can be used toward temporary or permanent mortgage rate buydowns.

This can lower monthly payments during the early years of ownership.

Consider Different Loan Products

Depending on your goals and time horizon, alternative financing options may make sense.

A trusted lender can help evaluate what fits your situation.

Look at Total Cost, Not Just Rate

Many buyers focus entirely on the interest rate.

While important, your monthly payment, home appreciation potential, tax benefits, and lifestyle improvements all contribute to the overall financial picture.

Be Ready When Opportunities Appear

Market conditions can shift quickly.

Having your financing, strategy, and search criteria ready allows you to act confidently when the right property becomes available.

What This Means for Buyers and Sellers in The Woodlands

For buyers and sellers in The Woodlands and surrounding communities, local market conditions often matter more than national headlines.

National inflation trends influence mortgage rates, but local inventory levels, buyer demand, and neighborhood-specific factors ultimately shape individual transactions.

At The McClung Group, we continually monitor both national economic trends and local market activity to help clients make informed decisions based on facts rather than fear.

Whether you're buying your first home, upgrading, downsizing, or exploring your options, having a strategy tailored to your goals is more valuable than trying to predict every economic headline.

Final Takeaway

Inflation has moved higher, and there's a realistic possibility the Federal Reserve could keep rates elevated or even increase them further before the end of 2026.

That may mean mortgage rates remain higher than many buyers were hoping for.

But higher rates do not automatically mean a housing crash, and they don't mean you should put your plans on hold indefinitely.

The housing market today is supported by stronger fundamentals, healthier homeowner equity positions, and tighter lending standards than we've seen in previous cycles.

The best move isn't always waiting.

It's understanding your options and making an informed decision based on your personal goals.

Ready to Talk About Your Next Move?

If you're wondering how rising inflation, mortgage rates, and local housing market trends could affect your plans, we'd love to help.

The McClung Group specializes in helping buyers and sellers navigate changing market conditions with confidence.

Schedule a call today and let's build a strategy that works for your goals, timeline, and budget.

Visit our website to connect with our team and start the conversation.

Tiffany McClung

Realtor and Team Leader | The McClung Group | Keller Williams The Woodlands & Magnolia

or another way